Key Takeaways

- Form 4506‑C rejections can happen for a variety of seemingly-trivial errors

- Common issues include mismatched names or TINs, outdated addresses, illegible scans, and missing or outdated signatures

- Formatting and data consistency are critical.

- Form 8821 is emerging as a better alternative, as it allows lenders or authorized third parties to directly access tax data through an ongoing authorization

- Form 8821 does not require the strict formatting of 4506-C, elimintating the bottleneck caused by frequent form rejections

Most IVES Form 4506‑C failures come from the same handful of avoidable mistakes, and for many lenders and small‑business borrowers.

4506-C failures can cause extensive delays to loan processing and contribute greatly to an institution’s ability to scale their process for growth.

4506-C failures can cause extensive delays to loan processing and contribute greatly to an institution’s ability to scale their process for growth.

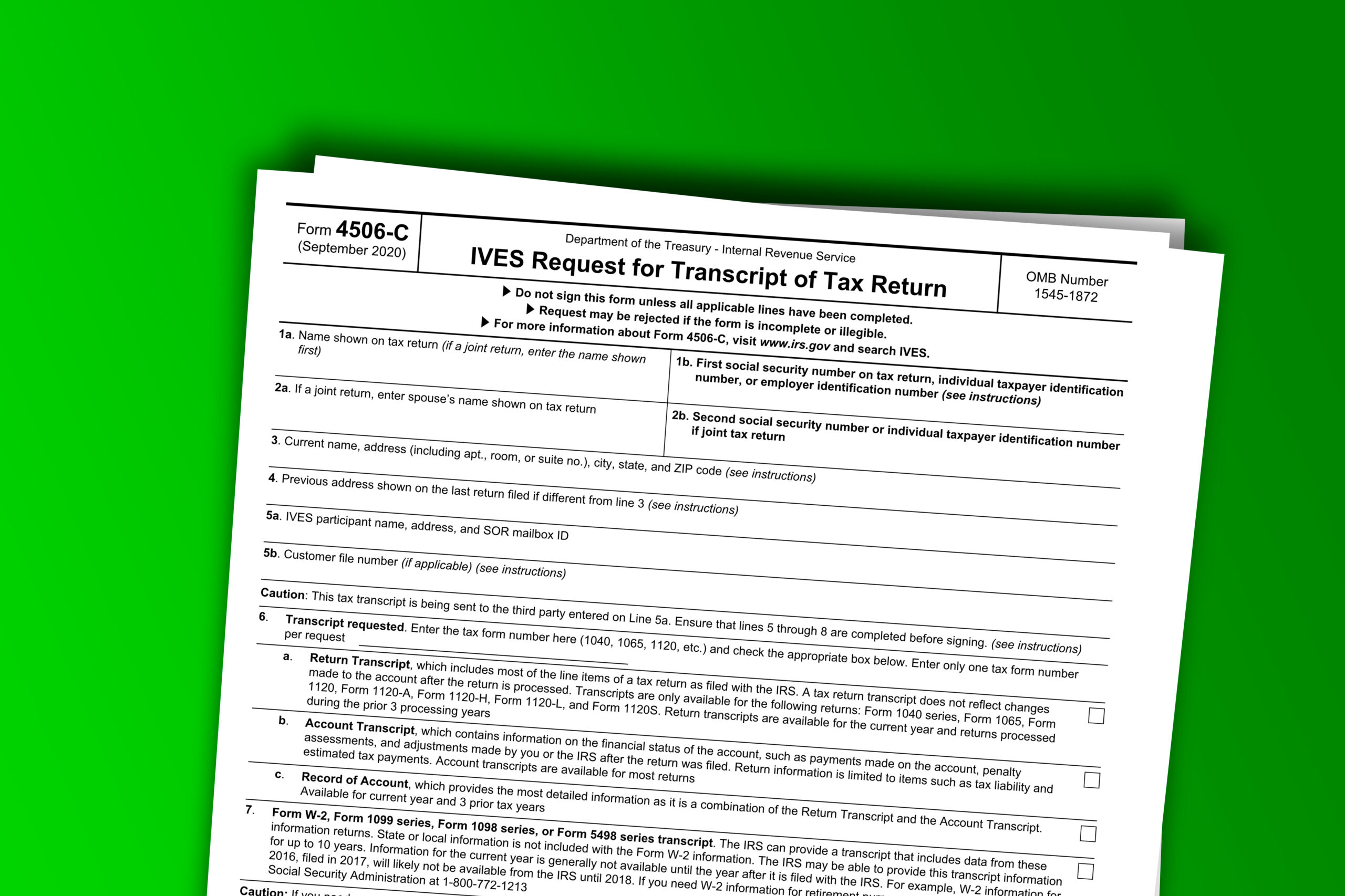

Why Your Transcript Keeps Getting Kicked Back

Many lenders use Form 4506-C to pull official IRS tax transcripts as part of underwriting and fraud prevention. However, strict formatting rules often result in rejected requests and a repeat of the process in order to access the needed transcripts.

1. Name and TIN Don't Match IRS Records

The first and biggest trip‑wire is identity mismatch. The IRS checks the names and taxpayer identification numbers on Form 4506‑C against what’s in its master file.

Common problems include:

From the borrower’s perspective, everything “looks right.” From the IRS’s perspective, the combination doesn’t match, and the system kicks the request back.

Common problems include:

- Using a nickname instead of the legal name on file

- Changing the order of spouses on a joint return

- Using an old business name after an entity has rebranded

- Typos in Social Security Numbers or EINs

From the borrower’s perspective, everything “looks right.” From the IRS’s perspective, the combination doesn’t match, and the system kicks the request back.

2. Address Mismatch With IRS Records

The address on Form 4506‑C must match the address associated with the tax return for the year(s) you’re requesting. This can include issues like:

The IRS uses the address fields to match the transcript request to the taxpayer’s account for specific periods. If it can’t reconcile the address, the request is rejected.

- The borrower provides a current address, but the IRS still has a different one on file for that year

- Missing apartment or suite numbers

- Multiple addresses listed in one line

- Illegible street names or city/state entries

The IRS uses the address fields to match the transcript request to the taxpayer’s account for specific periods. If it can’t reconcile the address, the request is rejected.

3. Old, Altered, or “Messy” Versions of the Form

In recent years, the IRS tightened rules around the format and cleanliness of Form 4506‑C to support automated scanning. Rejections frequently occur because:

To the lender it’s “good enough,” but to the system it’s noisy.

- The form is an outdated revision

- Fields show cross‑outs, white‑out, arrows, or handwritten corrections

- The form combines printed text, handwriting, and multiple fonts in a way the scanner can’t interpret

To the lender it’s “good enough,” but to the system it’s noisy.

4. Transcript Details Are Incomplete or Inconsistent

Line 6 and the transcript‑type checkboxes are another common failure point. Problems include:

When the IRS can’t tell exactly which transcript you’re asking for, it rejects the order.

- Leaving out the tax form number (for example, 1040, 1120, 1065)

- Listing multiple forms on a line when only one is allowed

- Checking the wrong transcript type box

- Writing tax years or periods in an unclear way or requesting periods that don’t exist

When the IRS can’t tell exactly which transcript you’re asking for, it rejects the order.

5. IVES Participant and Client Fields Not Filled Correctly

The IVES program depends on precise participant information to know where to send the transcript. Rejections happen when:

These fields must appear exactly as registered with IVES.

- The IVES participant name, address, or ID number is missing or incomplete

- The client/lender section is left blank or inconsistent with enrollment data

- Contact information is illegible

These fields must appear exactly as registered with IVES.

6. Signature, Authority, and Date Problems

Signatures are a major point of friction with this form. From the IRS side, there are clear rules:

If any signatures fail, the IRS cannot treat the form as a valid authorization and will not release transcripts.

- Signature or date is missing

- Signature doesn’t match the taxpayer (no documented authority)

- Wrong person signs for a business (unauthorized employee, incorrect title)

- Sign date is older than the allowed window (120 days) when the IRS receives it

- Non‑compliant electronic signature methods

If any signatures fail, the IRS cannot treat the form as a valid authorization and will not release transcripts.

7. Illegibility and OCR "Noise"

Even when every field is technically correct, the IRS can reject the request if the image quality is poor. Issues include:

Because IVES is highly automated, anything that confuses the scanner becomes a rejection.

- Low‑resolution scans or faxes

- Very light or very dark printing

- Skewed pages or heavy shadows

- Ink colors that don’t scan cleanly

Because IVES is highly automated, anything that confuses the scanner becomes a rejection.

The Cost of 4506-C Failure

In practice, Form 4506‑C is unforgiving. A mismatch in a name, address, or date can derail the entire request.

This is why many lenders are now looking at Form 8821 as a smarter, more flexible way to access tax data— one that’s better aligned with modern underwriting and portfolio monitoring needs.

From stalled closings, repeated “please re‑sign this form” emails, and frustrated borrowers who don’t understand why their clean tax returns are still under review, this is a bottleneck worth reversing.

This is why many lenders are now looking at Form 8821 as a smarter, more flexible way to access tax data— one that’s better aligned with modern underwriting and portfolio monitoring needs.

From stalled closings, repeated “please re‑sign this form” emails, and frustrated borrowers who don’t understand why their clean tax returns are still under review, this is a bottleneck worth reversing.

What Form 8821 Does

Form 8821 authorizes a third party to receive tax information directly from the IRS.

With a filed 8821:

Instead of chasing a new 4506‑C for every credit event, you have a standing permission tied to the IRS’s Centralized Authorization File (CAF).

With a filed 8821:

- The authorized party can access account information and tax return transcripts, usually through IRS online systems

- The authorization can cover multiple tax years and multiple tax types (individual, corporate, payroll, etc.) on one form

- The authorization remains in effect until it’s revoked or expires as specified, so you don’t need a fresh signature every time you need a transcript

- The authorization is “view-only access,” so clients don’t need to worry about how their sensitive information is being used

Instead of chasing a new 4506‑C for every credit event, you have a standing permission tied to the IRS’s Centralized Authorization File (CAF).

Why 8821 Reduces Friction

- Fewer form‑by‑form rejections: Once the IRS accepts the 8821 and loads it to CAF, future data pulls rely on the existing authorization instead of new, error‑prone 4506‑C forms.

- Ongoing visibility: Lenders can support renewals, annual reviews, and DSCR monitoring without repeatedly asking the borrower to sign new transcript forms.

- Broader data access: 8821 can authorize access not just to return transcripts but also to account data like balances, assessments, and certain notices—critical for understanding tax risk and cash‑flow impact.

Interested In Learning More About the Benefits of Form 8821?

Book a call with our team today to learn about how TOD can simplify your process, from transcript pulls to loan servicing and everything in between.